MARKET & PRICE TREND OF TUNGSTEN CHINA, 2021

PART VII of VII

Analysis of Subsequent Support for the Price of Tungsten’s Rising

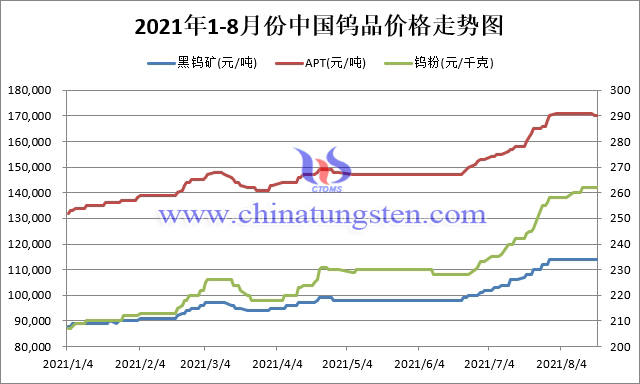

Since June this year, the price of tungsten products has continuously increased to about 15%, of which the price of tungsten concentrate has increased from RMB98,000 Yuan per ton to RMB114,000 Yuan per ton, an increase of 16.3%; The price of APT increased from RMB147,000 Yuan per ton to RMB 170,000 Yuan per ton an increase of 15.6%; The price of tungsten powder increased from RMB230 per kg to RMB260 per kg, an increase of 13.9%.

With several domestic leading enterprises with great influence in tungsten concentrate resources in tungsten industry, such as Xiamen Tungsten, Jiangxi Tungsten, Zhangyuan Tungsten and Xianglu Tungsten, the price of raw materials will remain high, and the price of tungsten products will remain at the current high level in the short term; Although the market has some fear of the current price, it is generally believed that the price of tungsten products will repeat the cycle of sharp rise and fall in the past. This is not a special case of the tungsten products market. All market emotions will have the game psychology of both long and short after the price rise, as is the case in the physical market, futures trading and stock market.

After analyzing the macro and meso economic trends, political and economic patterns, fiscal and financial policies and other factors at home and abroad, China Tungsten Online holds the opposite view on the analysis that the price of tungsten products in the industry will fall sharply. The author believes that the price of tungsten products will not fall sharply after this round of price rise, and will remain high for a long time, after that, there will be a greater possibility of rise. After the periodic rise, it will fall slightly from the first wave high in the early-stage next year and maintain the price as the normal market price.

Price Trend Chart of China's Tungsten Markets from Jan. to Aug. 2021

In late June 2021, China Tungsten Online made the first prediction for the current price rise of tungsten products, and made a deep analysis of the factors that made the rise. The relevant contents can be seen in the serial articles issued by the "Zhong Wei Online" official account. The 2021 market and price trend of tungsten products are restricted. As a follow-up development of the price rise, this paper intends to discuss the important support after the price rise of China's tungsten products in the second half of 2021, that is, the impact of the upcoming large-scale infrastructure wave in China, the United States and India on the tungsten products industry, clarify the market trend after the price rise of tungsten products, and boost the confidence in the price of tungsten products.

The basic logic of this paper is: on the one hand, from the consumer side, the consumption of tungsten products mainly comes from the consumption of industrial production and infrastructure construction, and the price of tungsten products is anchored to the difference between market supply and consumption, that is, the scarcity of tungsten products; Infrastructure construction will not only consume a lot of tungsten products such as cemented carbide, but also drive the demand for tungsten products in surrounding industries of steel, cement, glass and other building materials.

On the other hand, from the perspective of tungsten products industry chain, the demand for cemented carbide consumption, which accounts for the largest proportion of tungsten end consumer goods, increased due to the expansion of infrastructure investment, thus increasing the procurement of tungsten powder and tungsten carbide powder. The demand for powder pushed up the market consumption of tungsten chemicals, eventually leading to the flexible production and sales of raw materials such as tungsten concentrate and waste tungsten and maintaining high prices. Therefore, the focus of this paper is not the consumption trend of the industrial chain of tungsten products themselves, but the planning and investment trend of infrastructure investment in major economies in the world such as China, the United States and India in the future, so as to deduce that the price rise of tungsten products is not only due to market scarcity and the overall rise of material prices, The more firm and long-term supporting factor will be the demand for infrastructure construction.

Tungsten Metal Cube

1. Strong Growth of China's Infrastructure Demand for Tungsten Products

Generally speaking, infrastructure construction investment includes (1) traditional infrastructure construction, such as road transportation, municipal public facilities, power and heat investment, etc. (2) on the other hand, it also includes new infrastructure advocated in recent years, such as information infrastructure (5G, industrial Internet, Artificial Intelligence(AI), Augmented Reality(AR), Virtual Reality(VR), innovative infrastructure, such as the rise of industrial parks in various regions, (3) Meanwhile, we believe that the construction of smart city, technology city (future city), garden city, tourism and healthy City will be a new part of the comprehensive infrastructure, (4) the 2020-2021 year's continuous impact on COVID-19 will lead us to build up the public health software and hardware. For example, professional facilities such as medical institutions, emergency rescue and isolation treatment put forward higher requirements and faster construction speed, (5) after the great challenge of sudden natural disaster weather in Zhengzhou and other places in 2021, our infrastructure construction for urban and rural response to floods and other natural disasters will also become an important part of infrastructure construction, (6) in order to cope with the "Digital Dark Era", Such as the infrastructure construction of new energy vehicle charging station, communication facilities, general airport and emergency land and air transportation, as well as (7) the infrastructure construction of health, public health, sports and leisure in order to build a "Healthy China", and (8) the financial transfer payment and its landing project construction in order to achieve fair distribution and common prosperity.

Infrastructure is basically dominated by the government. Due to its large investment scale, long cycle and low new_, it often becomes the main means for the government to reverse regulate the economy and underpin the economic downturn. So, is there any pressure and demand to regulate economic growth and underpin the economic downturn in China?

The Related between GDP of China and the Price of Tungsten

The International Monetary Fund released the latest GDP growth rate of 8.1%, down 0.3% from the agency's previous forecast. Meanwhile, Goldman Sachs, JPMorgan Chase and Morgan Stanley lowered their GDP growth forecast for the third quarter from 4.3% to 2.0%, and the GDP growth forecast for the whole year from 9.1% to 8.9%, while the Chinese government's GDP forecast at the beginning of the year was about 6% relatively conservative. The IMF's latest forecast for the growth rate of US GDP this year will reach 7%, up 0.6% from the previous forecast of 6.2%. Through in-depth study of the reasons, from January to July 2021, the indicators of China's traditional "troika" driving economic growth are: investment increased by 10.3% year-on-year, with an average increase of 4.3% in two years; The total retail sales of social consumer goods increased by 20.7% year-on-year, with an average growth of 4.3% in the two years; The total import and export volume of goods increased by 24.5% year-on-year, with an average increase of 10.6% in the two years. These data show that the three indicators remain basically stable, only the import and export growth is rapid, and the overall trend is high in the first and low in the second; China's GDP grew by an average of 5.3% in the first half of the year, only 0.3 percentage points faster than that in the first quarter.

Apart from the stability of consumption, import and export, and the sluggish recovery of residents' consumption due to the emerging epidemic, the only thing that can significantly drive China's strong economic growth is infrastructure construction.

According to the general law, in the first year of each five-year plan, the central and provincial and local governments will promote some major projects one after another. This year is the first year of the implementation of China's 14th Five-Year-Plan. The construction of various industrial, agricultural and social infrastructure is imperative. Compared with the previous Five-Year-Pans, it is more urgent and requires more and larger infrastructure investment.

1.1 Reason: The Decline of Real Estate Makes Infrastructure the Main Tone of Investment

As the main investment option, the real estate market has been operating under the policy of no speculation in housing for more than two years. Various policies and measures to control house prices have been increasing in the near future. The main indicators of urban house prices and transaction volume represented by Shenzhen have decreased and shrunk significantly in varying degrees. In the medium and short term, the state will still strictly control real estate investment and house price speculation.

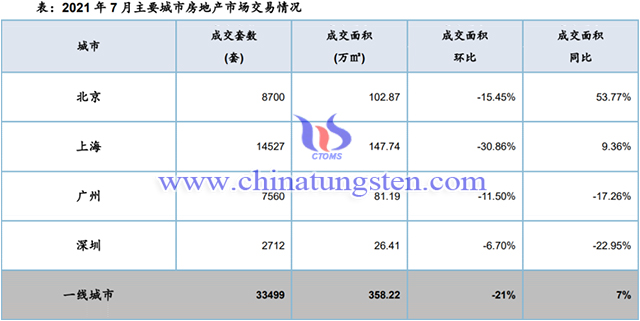

On July 30, the meeting of the Political Bureau of the CPC Central Committee continued to emphasize that "we should adhere to the positioning that houses are used for living rather than speculation, stabilize land prices, house prices and expectations, promote the steady and healthy development of the real estate market, accelerate the development of rental housing, and implement practical land, tax and other support policies". In May, the growth rate of residents' medium and long-term loans also began to decline. In June, the completed amount of real estate development investment was 1.79 trillion Yuan, with a year-on-year growth rate of 5.9%, falling for three consecutive months. In July, the sales area of commercial housing in 30 large and medium-sized cities was 17.16 million square meters, down 83000 square meters compared with the previous month, down 14.30% month on month. More than 80% of cities decreased in varying degrees, down 4.29% year-on-year, The transaction area of the four first tier cities fell month on month, of which Shanghai fell by more than 30% and Beijing by more than 15%.

On the other hand, in the past thirty years, infrastructure construction has provided a powerful impetus for the rapid economic growth of our country. The construction of the relatively advanced infrastructure, roads, bridges, port airports and high-speed rail has provided a strong guarantee for the balanced development of China's economy, and for the effective operation of COVID-19 and the effective supply of the supply chain and the economic viability. Therefore, the political and business circles generally believe that China's infrastructure investment in the second half of the year will be the best choice to maintain stable and rapid economic growth.

Real Estate Transactions in Major Cities of China in July 2021

1.2 Demand: The Necessity of a New Wave of Infrastructure Investment

(A) Demand for Short-term Policies to Support the Bottom and Maintain Stability

From 2020 to 2021, except that China's import and export will maintain rapid growth driven by the housing economy such as epidemic prevention materials, consumption and investment are not ideal. The central government determined a GDP growth plan of about 6% at the beginning of the year. It can be seen that the central government has an accurate judgment on the basic economic operation trend of this year. Therefore, we can infer that the state will timely launch a relatively positive fiscal policy in the second half of 2021, to ensure the basic stability and sustainable development of the national economy under the situation of strictly controlling the overheating of real estate. 7.30 the Politburo meeting stressed that the proactive fiscal policy should improve policy efficiency, hold the bottom line of "Three Guarantees" at the grass-roots level, reasonably grasp the progress of investment in the budget and the issuance of local government bonds, and promote the formation of physical workload at the end of this year and the beginning of next year. It should be a positive signal to vigorously promote the rapid promotion of infrastructure construction in the second half of the year, which can be predicted, Our Congress will withdraw from comprehensive measures such as finance and investment to ensure economic development in the near future.

(B) Rural Urbanization and Social Modernization

As of 2019, there is still a gap of more than 10 years between China's urbanization rate of 61% and that of Japan, the United States and major European developed countries. Urbanization will not only release a large number of rural labor force into industrial production and become a reliable human resource guarantee, but also continuously develop and upgrade China's agricultural intensification and industrialization; At the same time, rural urbanization will also make centralized and effective use of scarce resources such as education, medical treatment, heating and sanitation in China's vast rural areas, balance the gap between urban and rural modernization, improve the overall modernization of society, and realize a more equitable distribution and sharing of social wealth and resources, It also provides a material basis for the smooth realization of China's carbon neutralization goal of energy conservation and carbon reduction in 2060. China's vast rural urbanization and modernization process will greatly promote the demand and construction of economic and social infrastructure.

(C) One Belt, One Road Infrastructure Needs

One Belt, One Road, has been tested since 2020. COVID-19 has demonstrated the foresight, necessity and urgency of the construction of the whole area. In terms of sea and air transportation, a large number of China's export goods have encountered unprecedented sea transportation congestion and a ten-fold increase in freight rates. Air transportation has encountered a series of problems, such as limited transport capacity, insufficient routes, limited airport handling capacity and high freight rates, and the sea and air will be affected by geopolitical and social risks at any time One Belt, One Road port, will be built up and expanded in the future.

Infrastructure Construction

Recently, the situation in Afghanistan in the southeast of China has taken a sharp turn for the worse and has become predictably stable. The obvious friendly policy towards China of the new Afghan government will give China the opportunity to participate in reconstruction, alleviate the security pressure on China Pakistan Economic Corridor, and improve the value of the port in Guadar, Balochistan province, Pakistan, Therefore, China is expected to take advantage of the favorable opportunity of Afghanistan's reconstruction and economic recovery to expand and expand the construction of China Pakistan Economic Corridor.

China’s One Belt, One Road, will probably follow the Central Asian and the Middle East across the Suez Canal in Egypt, and link the Tanzania Railway - the Mombasa-Nairobi Railway and the Dapilon-Santou Railway to the world's largest iron ore in the Republic of Guinea, (La République de Guinée)which is opened by China’s Compnaies, and then directly link the copper, iron, and land through the land route. The withdrawal of the United States is scheduled to withdraw from Syria and withdraw from Liberia. One Belt, One Road, is not a dream. So, the near future and the whole area of infrastructure construction will not only promote the development of various industries in China, but also bring rich resources to our country.

To the south, under the background that Malacca is controlled by the United States and the South China Sea is still unstable, climate warming makes the Arctic route to Europe through Russia and countries in the Arctic circle a maritime transport channel of great strategic value and economic significance. The friendly cooperative relations and economic complementarily between China and Russia, China's strong infrastructure capacity and economic strength, and huge maritime demand, it will enable China to further pay more attention to Arctic routes and relevant infrastructure investment such as land, sea and airport.

Types of Logistics

One Belt, One Road with a unique advantage of stability, efficiency, wide coverage, all day long, and no influence on air and sea transportation, highlights the importance of the construction of the whole area. It has also become a weapon to solve the dilemma of "one cabin is hard to find" and "one box is hard to find". Since May 2020, China-Europe trains have operated more than 1000 trains in a single month for 15 consecutive months. Since May this year, more than 1300 trains have been operated in a single month for three consecutive months. In July, the operation quality of China Europe trains continued to improve. 1352 trains and 131000 TEUs of goods were operated in the whole month, with a year-on-year increase of 8% and 15% respectively.

China-Europe trains directly transported to European countries, improving the timeliness of goods transportation, it saves time and storage costs, improves the turnover rate of freight and container capacity, and effectively ensures the stability and smoothness of the international industrial chain supply chain. However, One Belt, One Road, is also a key factor in the extreme weather. The central European train has been exposed to the adverse effects of floods and floods in Zhengzhou and other places. This is a short way to deal with extreme weather such as power, scheduling, communications and other infrastructure. Therefore, as a representative of the whole area, China's infrastructure along the line should have more input and more lines, and will gradually combine with air and sea transportation to Africa and South-Central America. This will be a major infrastructure construction affecting the world.

(D) Infrastructure Short Board Construction Demand

At the beginning of reform and opening up, China put forward the slogan of "Building Roads Before Getting Rich". It has been committed to improving infrastructure construction and serving economic development. Since 2008, it has been speeding up. After more than ten years of efforts, China's expressways, high-speed railways, hydropower, nuclear power, solar energy, wind energy and communication base stations are among the forefront in the world, However, the advantage and leading position of the total amount is that on the one hand, compared with the economies of the United States, Japan, Germany, Britain, France and Russia, China's per capita infrastructure is relatively backward. Just as China's total economic volume ranks among the top in the world, but its per capita GDP lags far behind the developed economies in the world, there is still a big gap in China's per capita infrastructure, especially in the central and western regions, There is still much room for improvement and more long-term infrastructure investment is needed.

The epidemic since 2020 has put China's logistics and supply chain system through a severe test, proving China's unique global industrial production capacity and the resilience of the supply chain system, but it also highlights many problems, such as insufficient infrastructure, operation capacity and intelligence such as sea and air ports; The worldwide extreme weather since 2021 has verified many problems and lessons in the process of China's rapid urbanization, such as urban flood drainage, public health and emergency rescue, rural flood and waterlogging natural disasters, etc. the problems exposed in Zhengzhou, Henan Province will not only put forward new topics for the future urban construction planning, It also puts forward requirements for us to improve and improve urban infrastructure and emergency system in the short term. Therefore, we have reason to believe that our Congress is facing the construction and improvement of emergency systems such as roads, power supply, telecommunications and public health in cities and villages.

In order to achieve the goal of carbon neutralization by 2060 and environmental protection measures such as energy conservation and emission reduction, China is currently investing in more hydropower projects and photovoltaic power stations in the central and western regions, and building wind power stations in suitable areas throughout the country. In terms of nuclear power construction, in addition to coastal areas, China is trying to invest in more nuclear power facilities in inland areas, such as West to east gas transmission UHV power transmission and transformation projects are also gradually promoted, and China's natural gas projects introduced from the Middle East and Russia are gradually applied nationwide. Therefore, more new energy projects, new energy supply modes and channel construction will steadily promote the development of China's infrastructure construction for a long time.

China’s New Energy Construction

1.3 Experience: Thinking & Experience of Advanced Deployment of Infrastructure

In the 1998 financial crisis, China successfully played the image of a responsible big country after recovering Hong Kong in 1997. Instead of devaluing the RMB, China provided $4 billion in aid to Thailand and other Southeast Asian countries. On the one hand, the government adopted the policy of expanding domestic demand for education, medical treatment and real estate to stimulate economic growth, maintaining the healthy and stable growth of the domestic economy, it has played an important role in easing Asian economic tensions and driving Asian economic recovery.

During the economic crisis in 2008, China took advantage of the situation and resolutely invested $4 trillion in infrastructure construction. At that time, many Chinese people and media generally believed that the construction of high-speed railway projects was too advanced. However, China realized the problems and difficulties of rapid export growth at the time of global crisis, and then increased bank loans on a large scale and invested heavily in the construction of "railway infrastructure", It invested in the construction of new and expanded industrial development zones and other infrastructure, and actively promoted China's capital investment represented by state-owned enterprises to acquire global mineral resources trapped by the international crisis, so that China can survive the global crisis and further enhance its industrial production and resource self-sufficiency.

Since 2020, the United States has been increasing the speed of printing money to boost the economy and maintain basic social stability by issuing more money. However, the effect of boosting production and consumption is not good, but the negative effect is the popularity of American real estate and soaring prices. According to the data released by the American Association of real estate agents on August 12, the median sales price of existing homes in the United States reached US $357900 in the second quarter, with a year-on-year increase of 22.9%, the largest increase in the same period in 53 years since 1968. Meanwhile, the US CPI in July rose by 5.4% over the same period last year, the largest single month year-on-year increase since 2008.

It can be seen that the inflation in the United States has been very serious, which proves that the large-scale printing of money in the United States did not flow to the real economy, but greatly pushed up the prices of real estate and food. China holds a large number of US bonds and has a large amount of foreign exchange reserves. After we see the consequences of US inflation and the current situation of its own economic slowdown, expanding infrastructure investment and large-scale infrastructure investment to meet China's current and future actual needs may be the best option to deal with another wave of economic crisis.

1.4 Support: Financial Basis for Infrastructure Development & Stability Maintenance

In the first half of 2021, due to the strong recovery of overseas demand after the epidemic, driving China's strong exports and strong support for economic growth, China's fiscal and monetary policies are conservative. However, with the continuous emergence of the trend of high before low, the downward pressure on the economy will increase in the second half of the year, and the domestic fiscal and monetary policies are expected to further exert force. It is difficult to effectively boost consumption and weaken overseas demand, Under the strict control of real estate, infrastructure investment will soon enter another climax.

China’s Infrastructure Construction

The conservative strategy of bond issuance and fiscal expenditure in the first half of the year also gives more room for policies in the second half of the year. In the first half of the year, the year-on-year growth rate of social finance and M2 continued to decline. In June, the year-on-year growth rate of social finance stock was 11%, and the year-on-year growth rate of M2 was 8.6%, which has remained downward since November last year. In 2021, the national debt limit is 2.75 trillion Yuan, the general debt limit of local governments is 0.8 trillion Yuan, and the special debt limit is 3.65 trillion Yuan. The total of the three is about 7.22 trillion Yuan. From January to July, the cumulative issuance of national debt and government bonds is 2.71 trillion Yuan, with an issuance progress of 38%. There is still a huge elastic space of 4.5 trillion Yuan in fiscal force in the second half of the year, we expect that the progress of financial bond issuance and expenditure and project implementation will be accelerated in the second half of the year, forming the key to financial underpinning and economic growth. Financial bond issuance and expenditure will invest more in infrastructure projects, quickly form physical workload, and infrastructure investment will form a small hot wave from September to October. 7 .30 the meeting of the Politburo stressed that the setting tone of physical workload will be formed at the end of 2021 and the beginning of 2022. The third quarter is the most convenient season for engineering construction in a year. It can be predicted that China will invest more in infrastructure construction and build at a higher speed in the second half of 2021.

2. Prelude to Large-scale International Infrastructure Investment

2.1 US Infrastructure Investment

Compared with China and the United States, it is mainly reflected in the reasons why the U.S. economy is optimistic in the second half of the year, mainly due to the monetary release of the Federal Reserve and the large-scale economic stimulus plan and infrastructure plan of the U.S. government. Over the past year, the Federal Reserve's money gate has opened wide and injected more than $400 billion into the market. The trillions of dollars of U.S. economic stimulus plan and infrastructure plan will have some practical effects. This may be one of the reasons why institutions are optimistic about the U.S. economy. In this context, on August 10, the US Senate passed an infrastructure investment bill with a total amount of about US $1 trillion. At the same time, it has a budget plan of up to US $3.5 trillion involving priority issues such as health care, child and elderly care, education and climate change. Although the relationship between the two parties in the United States is sharply opposed, the society is seriously torn, and the political ecology is deteriorating. It is unknown how much and how long these broad investment plans can be realized in the political environment of low social efficiency in the United States, these huge plans are ultimately the ambitious economic stimulus policy of the Biden administration, it will certainly bring great benefits to global infrastructure related industries.

2.2 Infrastructure in India

Indian Prime Minister Modi announced on August 15 that he plans to invest 100 trillion rupees (about 8.73 trillion Yuan) in the country's infrastructure to promote economic growth and create jobs. These investments will be used in India's transportation and logistics industry, integrate transportation modes, improve domestic supply chains and connect to international supply chains. At the same time, Modi government also set the goal of achieving energy independence by 2047, He said the goal could be achieved by promoting electric vehicles, turning to a natural gas-based economy and building a hydrogen production center. "This will help reduce domestic travel time and increase industrial productivity, help India's industry become globally competitive and develop economic zones." although there are no details of the Indian government's huge infrastructure and its implementation efficiency, in any case, they are aware of the infrastructure gap with other countries, especially China, It is believed that even the greatly discounted infrastructure plan will greatly boost the export of China's cemented carbide to India, a traditional market.

2.3 Infrastructure in Other Countries

When extreme weather became the norm around the world, the Nordic countries first tasted the pain. On July 13, Seblitz, Germany, suffered a serious disaster caused by rainfall and flood, which killed at least 180 people and left 150 missing. Then, German President Steinmeier said that the reconstruction funds for the flood were expected to reach billions of euros. The huge climate disaster makes people realize that it is not only necessary to invest more capital construction funds, but also to fundamentally change the original production, life and travel modes, and invest more resources in energy conservation and carbon reduction, new energy application and other infrastructure, so as to gradually reduce carbon emissions and natural disasters. We can foresee that in the post epidemic era, the countries of the world should not only reconsider the infrastructure construction of their industrial production and supply chain, but also need to invest more resources in public health facilities such as medical treatment to deal with the similar public crises that COVID-19 has not yet completed and may erupt at any time.

3. Conclusion: The Global Infrastructure Tide Will Maintain the Stability of Tungsten Price

In conclusion, we believe that a new round of global infrastructure construction represented by China, the United States and India will bring a new round of rapid growth to China's tungsten industry, put forward higher quantitative and quality requirements for our tungsten products industry, and pose challenges in forming a more flexible and efficient tungsten products production and intelligent supply chain system on the basis of energy conservation and carbon reduction, At the same time, it will also bring stable price and profit expectation of tungsten products in China.

In the international market, the original inventory of tungsten products is about to be exhausted. In the second half of 2021, when a new round of replenishment is about to begin, we have reason to expect a stable rise in the demand and price of tungsten products.

------------The End------------

Read/download the full report: